Emergency Funds 101: The Key to Staying Debt Free and Sane

January 25, 2023

The pandemic taught us many things. Perhaps one of the most indelible is the importance of having an emergency fund for whatever life throws at us. If you’re still recovering from the financial fallout of COVID, saving for a future emergency may still seem like a distant dream for “one of these days” — but there are creative ways to start adding to your stash now that won’t impact your daily life, even when times are tight.

Emergencies don’t announce their pending arrival months in advance. They pop up unexpectedly and trigger a mad scramble for cash to cover whatever catastrophe (faulty plumbing, a distracted teen driver or novice laser hair removal technician) fate may have in store. Enter the financial world’s most often-cited insurance policy: The emergency fund.

Here’s a look at everything you need to know about emergency funds — how much you need, strategic ways to save, where to stash your cash — so you can understand why they hold the key to staying debt free and sane during extremely challenging times.

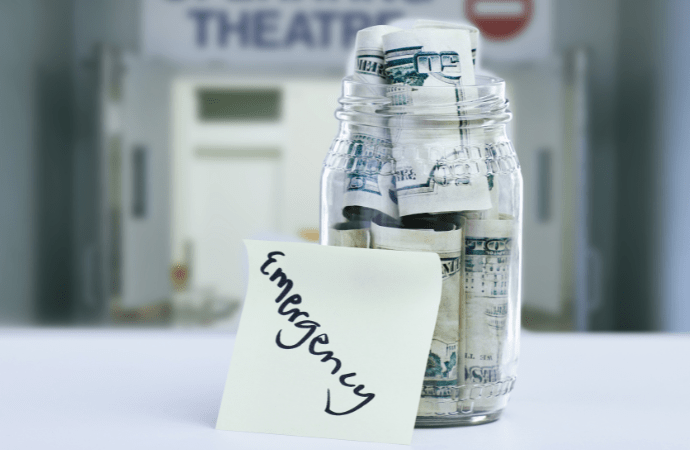

What is an emergency fund?

An emergency fund is a pool of money earmarked for surprise expenses that fall outside of your regular budget. It’s a financial safety net — a rainy-day fund — so you don’t have to run up a balance on a high-interest credit card, tap into your home equity or withdraw money from retirement savings or the kids’ college funds to pay for the unexpected. (It’s difficult enough to face an expensive emergency as it is, but ending up in credit card debt afterwards just adds insult to injury, which is why an emergency fund is so important.)

The money in your emergency fund can be used to cover unexpected expenses (like a leaky roof) just as easily as it can be used to cover your essential expenses in the event that you lose your job. Essential living expenses include rent/mortgage, food, insurance premiums and gas money to get to and from places you need to go. (Non-essentials would be cable, salon visits, tickets to sporting events, etc.)

Why you really need an emergency fund

Emergencies can impact anyone, but the financial fallout is potentially much more severe and prolonged when you don’t have a cushion to soften the blow. The bottom line: Everyone needs a stash of cash you can get your hands on when the you-know-what hits the fan (as it inevitably will when you least expect it).

Exactly how much should I have saved in an emergency fund?

So, how much do you need? The size of your financial safety net depends on whether you have dependents, whether you’re the sole (or primary) breadwinner, or whether you have access to other money. Although it’s good to build up your emergency fund to cover six months’ worth of fixed living expenses, if you don’t have anywhere near that, don’t fret. New research shows that six weeks’ of living expenses is a perfectly adequate emergency savings goal.

Don’t know where to start? Then start with the goal of saving $2,000. Do that, and you’ll have achieved a savings milestone that half of all Americans have not yet reached. Here are a few other savings guidelines:

- If even six weeks of savings seems impossible…set a manageable weekly savings goal — $10, $20, $50 or whatever amount you can afford — and just get the ball rolling. Set up an automatic transfer on payday to funnel whatever you can spare into a separate account (one of the ones we recommend below) so you never notice the money was ever there. When you’ve amassed several hundred dollars, set your sights on that $2,000 goal.

- If you’re retired … The prudent move is to have enough cash on hand to cover one year of expenses and another chunk to cover three years of living less liquid, but still sheltered from the whims of the stock market. That latter chunk can remain in your retirement account until you need to use it.

- If you’re single or the sole earner in your household … you need a larger emergency fund (think double) than a two-income couple (where one partner’s salary can provide a temporary financial bridge).

- If you’ve got competing savings goals … split the difference. For example, if you’re currently saving 10% of your income, funnel 3% into an emergency fund and 7% into long-term savings until your rainy-day fund is whole. (Pro tip: If your employer matches a portion of your 401(k) contributions, take full advantage of that as you’re building your emergency fund.)

Where to stash your cash

You want to keep your emergency fund separate from your regular spending money in an account that’s safe, liquid and earning the highest rate of return possible without putting your money at risk. Think of a high-yield savings account, money market account, or savings certificates available from your credit union. These are all extremely low risk and NCUA-insured. Even a Roth IRA can serve as an emergency source of cash when necessary, and help grow your retirement savings if you don’t need to tap into the account early.

Where not to stash your cash

You want your emergency fund to be safe from potential losses, so it shouldn’t be in the stock market, where short-term fluctuations might make it take a dip. You also want your emergency fund to be accessible, but not too accessible. That’s why it belongs in an account different from your regular savings account — so that you won’t be tempted to touch the money unless you really need it. If you look for a high-yield savings account, you’ll find that they generally dish out higher interest rates than you’ll get from a traditional bank — close to 20 times more. But with any financial product, make sure you read the fine print.

PPP Forgiveness Application Deadline

Congress passed The Economic Aid Act which changed the deferment period from 6 months post covered period to 10 months post covered period. For example, if your covered period ended June 30, 2021, under the new guidelines the earliest your first loan payment wouldn’t be due until April 2022, and you have until then to request forgiveness. Please use the following calculation to help you identify when your forgiveness will be due:

- PPP borrowers may select a covered period anywhere from 8 weeks to 24 weeks.

- RCU is automatically calculating your loan due date based on a 24-week covered period, if you intend on using a shorter covered period please inform us immediately as this will impact your due date.

- Your correct deadline will be reflected in your online banking account.

If all or part of your PPP loan is not forgiven, your first loan payment will be due the first of the following month after a decision is made by the SBA.

Leaving Our Website

You are leaving our website and linking to an alternative website not operated by us. Redwood Credit Union does not endorse or guarantee the products, information, or recommendations provided by third-party vendors or third-party linked sites.