Why Is Money So Emotional?

February 4, 2023

While our finances can stress us out, there are ways to take control

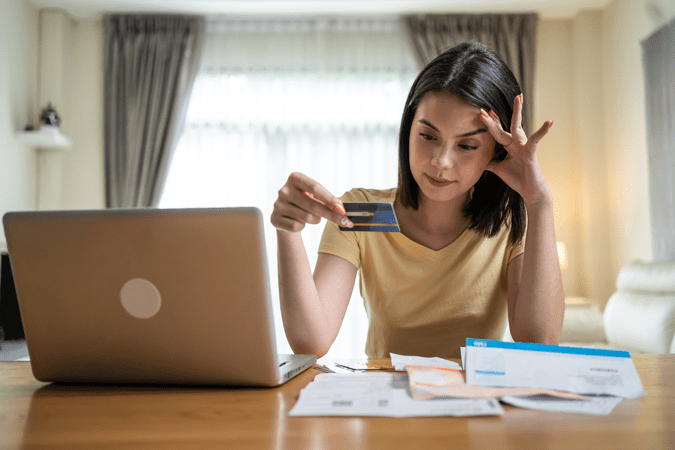

Anyone who has ever lost sleep over credit card bills or stock market shake-ups knows that money is so much more than just a set of numbers on a screen. Money, or a lack of it, can be fraught with emotions that – in some cases – lead to health issues including anxiety and depression.

A 2022 survey on money and mental health from Bankrate and Psych Central showed that a large number of Americans experience financial worries. Among those polled, 42% say concerns about finances are having a negative impact on their mental well-being. Between the aftershocks of a global health pandemic and the daily struggles sparked by sky-high inflation, it’s more than understandable.

Other factors could be at work, too. People have emotional attachments to their money because of growing up in poverty (or wealth), experiencing a job loss, or a variety of other issues that don’t always surface without deliberate self reflection. Because we are not always aware of the internal causes of our money issues, breaking through the emotional challenges surrounding them can be difficult. But it’s not impossible. It just requires taking the time — and making the effort — to identify the emotional triggers that can sabotage your financial life. Ideally, that awareness can lead to positive behavioral changes that lead to a less-stressful future when it comes to handling money.

If you need help working through the process, such as identifying the things that take you off track, a financial counselor may be able to assist. While financial planners address the more matter-of-fact aspects of money management, financial counselors tackle money issues through more of a life-coach approach. Many are not licensed psychotherapists (although financial therapists are an option as well) and not all are certified financial planners. These professionals work to help clients understand the root causes of their money troubles and assist them with developing ways to alter or overcome unhealthy financial behaviors.

Launch a path to progress

We all have different experiences with money that led us to where we are now. If you’re wondering what yours are, the free MoneyType quiz developed by Jennifer Leigh Selig, PhD is a great place to start. The good news is that with some guidance, you have the power and ability to change. Here are some strategies to help in overcoming the negative emotions that can sideline our financial progress:

- Know where you are: A study from budgeting app Mint shows that 65% of Americans don’t know how much money they spent last month. That can be a problem when you want to set yourself up for financial success in the future. So, if you are among the 35% of Americans who regularly track your spending, congrats! If not, grab your financial statements and dive in. (And, if you need some help with this, check out the next session of FinanceFixx, a new coaching program from HerMoney’s Jean Chatzky.) Make sure to take a hard look at all checking and saving account records, credit card bills, and the other ways you spend including ATM withdrawals, Venmo, Paypal, etc. Hopefully the number is less than the amount you earned. If not, it’s time to make adjustments. That could mean less take-out in favor of more meals at home. Or, reducing the number of subscription services you have (the average American has 24!) Clearly, there’s room to trim.

- Know exactly where you’re headed: Financial counselors and therapists emphasize how important it is to not deal in hypotheticals. That means you should make sure to get it all down on paper or in a digital spreadsheet — everything from your current financial status to the specific goals you want to achieve.

- Build a budget: Creating a budget for your money can help take the emotion out of your spending and savings habits. In fact, people who actively use a budget often save more than those who don’t. If the ‘B’ word sends shivers down your spine, think of it as a roadmap to where you want to be in the future. And make it easy on yourself. Go online and type in ‘budget apps’ to see which type of tracking system may work best for you. But make no mistake, you need a budget.

- Put a plan in place: Once you have a budget and you know where your money needs to go, set your finances on autopilot as much as possible. That could mean making automatic monthly debt payments (think your mortgage or car loan) or having automatic transfers deducted from your checking account every few weeks into an emergency fund such as a high-yield savings account at your credit union. One of Jean Chatzky’s favorite money rules is #11: “If you can’t see it and you can’t touch it, you won’t spend it.”

- Schedule regular check-ins: As with any challenging subject, getting better with money takes practice. During a weekly check-in, you can review your online bill payments, go over your expenses, reconcile your checkbook or deal with sticky issues you’ve been avoiding. Set a timer for 30 minutes and continue working on money matters until the buzzer goes off. When you get the hang of it and find it only takes a few minutes to make sure everything is in order, you can cut your check-ins back to every two weeks.

- Seek assistance: Finally, remember there’s no need to struggle through a challenging situation alone. Help is available for those who need it. The Association for Financial Counseling & Planned Education and the Financial Therapy Association have searchable directories of practitioners. Some have a background in psychology or counseling while others are from the financial advice space. Many should offer a free initial consultation to see if you are a good fit.

We’re here for you

Visit our Financial Wellness Resource page to get more information on the topics that resonate with you, or sign up for one-on-one coaching with our partners at BALANCE.

Want more? Here’s some additional ways to cope with financial stress.

PPP Forgiveness Application Deadline

Congress passed The Economic Aid Act which changed the deferment period from 6 months post covered period to 10 months post covered period. For example, if your covered period ended June 30, 2021, under the new guidelines the earliest your first loan payment wouldn’t be due until April 2022, and you have until then to request forgiveness. Please use the following calculation to help you identify when your forgiveness will be due:

- PPP borrowers may select a covered period anywhere from 8 weeks to 24 weeks.

- RCU is automatically calculating your loan due date based on a 24-week covered period, if you intend on using a shorter covered period please inform us immediately as this will impact your due date.

- Your correct deadline will be reflected in your online banking account.

If all or part of your PPP loan is not forgiven, your first loan payment will be due the first of the following month after a decision is made by the SBA.

Leaving Our Website

You are leaving our website and linking to an alternative website not operated by us. Redwood Credit Union does not endorse or guarantee the products, information, or recommendations provided by third-party vendors or third-party linked sites.