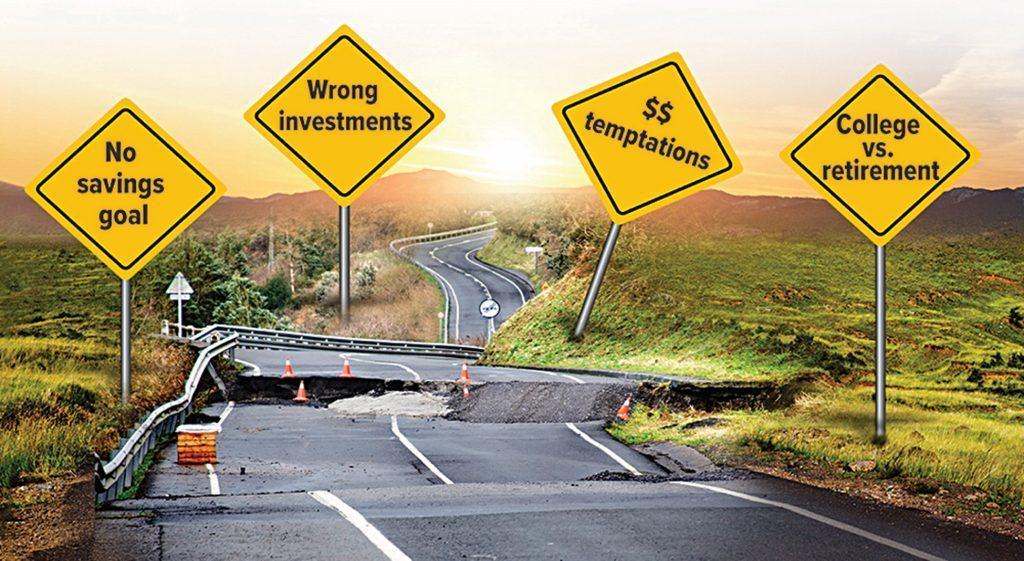

Watch for These Hazards on the Road to Retirement

July 18, 2024

On the road to retirement, be on the lookout for hazards that can hamper your progress. Here are five potential risks that can slow you down.

Traveling aimlessly

Embarking on an adventure without a destination can be exciting, but not when it comes to retirement. Before starting any investing journey, the first step is setting a realistic goal. You’ll need to consider a number of factors — your desired lifestyle, salary/income, health, future Social Security benefits, any traditional pension benefits you or your spouse may be entitled to, and others. Examining your personal situation both now and in the future will help you home in on a target.

While some people prefer to establish a lump-sum goal amount — for example, $1 million or more — others find a large number daunting. Another option is to focus on how much you might need on a monthly basis during retirement. Regardless of the approach taken, be sure to factor in inflation, which can place unexpected curves in your path.

Investing too aggressively…

You may also encounter potholes when trying to target an appropriate rate of return. Retirement investors aiming for the highest possible returns might want to overweight their portfolio in the most aggressive — and risky — investments available. Although it’s generally wise to invest at least some of a retirement portfolio in higher-risk investments to help outpace inflation, the proportion and individual investment selections should be determined strategically. Investments seeking to achieve higher returns involve a higher degree of risk. Appropriate decisions will reflect your goal, your investment time horizon, and your general ability to withstand volatility.

Proceed with Caution

…Or too conservatively

On the other hand, if you’re afraid of losing any money at all, you might favor the most conservative investments, which strive to protect principal. Yet investing too conservatively can also be risky. If your portfolio does not earn enough, you may fall short of your goal and end up with a far different retirement lifestyle than you originally.

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful.

Giving in to temptation

Most people experience an unplanned detour on the road to retirement — the need for a new car, an unexpected home repair, an unforeseen medical expense, or the opportunity to take a long, exotic vacation.

During these times, your retirement portfolio may loom as a potential source of funding. But think twice before tapping these assets, particularly if the money is in a tax-deferred account such as an employer-sponsored plan or IRA. Consider that:

- Any dollars you remove from your portfolio will no longer be working for your future.

- In most cases, you will generally have to pay regular income taxes on amounts that represent tax-deferred investment dollars and earnings.

- If you’re under age 59½, you may have to pay an additional penalty of 10% to 25%, depending on the type of retirement plan and other factors (some emergency exceptions apply — check with your plan or IRA administrator).

It’s best to carefully consider all other options before using money earmarked for retirement.

Prioritizing college over retirement

Many well-meaning parents may feel that saving for their children’s college education should be a higher priority than saving for their own retirement. “We can continue working as long as needed,” or “our home will fund our retirement,” are common beliefs. However, these can be very risky trains of thought. While no parent wants his or her children to take on a heavy debt burden to pay for education, loans are a common and realistic college-funding option — not so for retirement. If saving for both college and retirement seems impossible, a financial professional can help you explore a variety of tools and options to assist you in balancing both goals (however, there is no assurance that working with a financial professional will improve investment results).

*Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2024. Non-deposit investment products and services are offered through CUSO Financial Services, L.P. (“CFS”), a registered broker-dealer (Member FINRA/SIPC) and SEC Registered Investment Advisor. Products offered through CFS: are not NCUA/NCUSIF or otherwise federally insured, are not guarantees or obligations of the credit union, and may involve investment risk including possible loss of principal. Investment Representatives are registered through CFS. The credit union has contracted with CFS to make non-deposit investment products and services available to credit union Members. SEC Marketing Disclosure.

PPP Forgiveness Application Deadline

Congress passed The Economic Aid Act which changed the deferment period from 6 months post covered period to 10 months post covered period. For example, if your covered period ended June 30, 2021, under the new guidelines the earliest your first loan payment wouldn’t be due until April 2022, and you have until then to request forgiveness. Please use the following calculation to help you identify when your forgiveness will be due:

- PPP borrowers may select a covered period anywhere from 8 weeks to 24 weeks.

- RCU is automatically calculating your loan due date based on a 24-week covered period, if you intend on using a shorter covered period please inform us immediately as this will impact your due date.

- Your correct deadline will be reflected in your online banking account.

If all or part of your PPP loan is not forgiven, your first loan payment will be due the first of the following month after a decision is made by the SBA.

Leaving Our Website

You are leaving our website and linking to an alternative website not operated by us. Redwood Credit Union does not endorse or guarantee the products, information, or recommendations provided by third-party vendors or third-party linked sites.